In recent years, Pakistan, Egypt, and Argentina have faced significant economic challenges, with debt management becoming a central issue. These three nations, though separated by geography, share similarities in their economic struggles, particularly in terms of external debt, fiscal deficits, inflation, and currency devaluation. This article explores the comparative debt positions of Pakistan, Egypt, and Argentina, evaluating the economic situations that have led to their current predicaments and examining the commonalities in their financial crises.

Debt Overview: Pakistan, Egypt, and Argentina

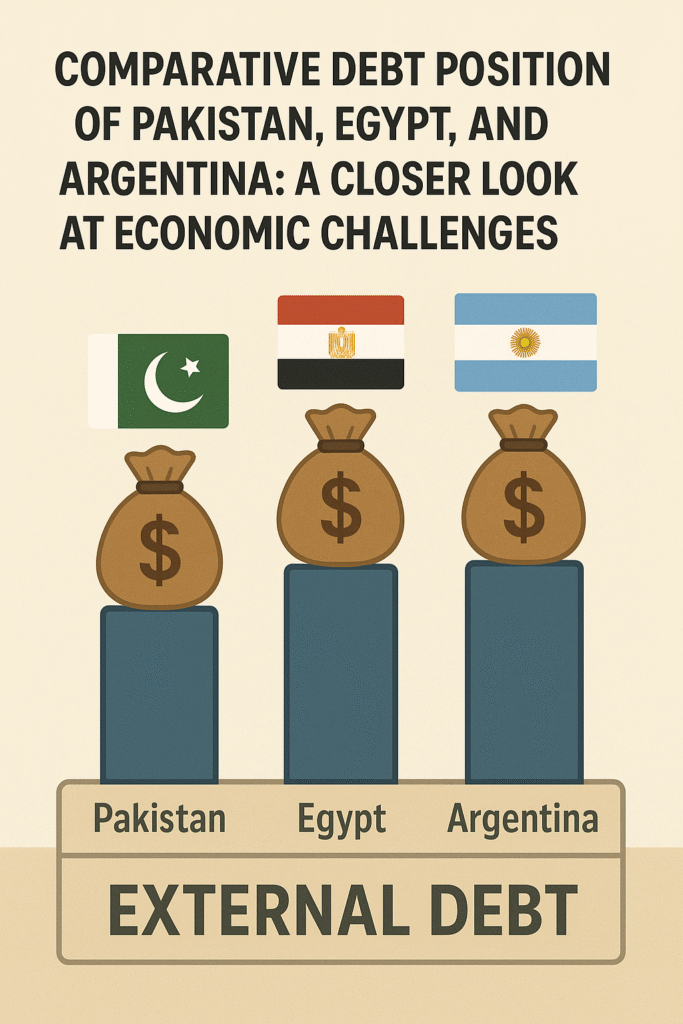

1. Pakistan:

– Total External Debt (2024): Over $125 billion

– Debt-to-GDP Ratio: Approximately 80%

– Key Issues: High reliance on external financing, recurring balance of payments crises, and a heavy dependence on international financial institutions (e.g., IMF).

2. Egypt:

– Total External Debt (2024): Around $165 billion

– Debt-to-GDP Ratio: About 90%

– Key Issues: Significant public sector debt, large fiscal deficits, and a reliance on external borrowing to finance mega-projects and maintain foreign reserves.

3. Argentina:

– Total External Debt (2024): Over $190 billion

– Debt-to-GDP Ratio: Exceeding 80%

– Key Issues: History of sovereign defaults, high inflation, currency instability, and recurring debt renegotiations with international creditors.

These countries have accumulated substantial external debt over the years, driven by a combination of domestic economic weaknesses, global economic trends, and, in many cases, unsustainable government spending. Although their debt positions vary in absolute terms, the underlying economic issues have created a vicious cycle of borrowing and repayment difficulties.

Similarities in Economic Situations

1. Reliance on External Financing and the IMF:

One of the most significant similarities among Pakistan, Egypt, and Argentina is their heavy reliance on external financing, particularly from international financial institutions such as the International Monetary Fund (IMF). All three countries have engaged in multiple loan programs with the IMF, often as a last resort to avoid default and stabilize their economies.

– Pakistan: Since 1988, Pakistan has entered into more than 20 agreements with the IMF. The most recent program, signed in 2023, aimed to address a severe balance of payments crisis, stabilize foreign exchange reserves, and implement structural reforms.

– Egypt: Egypt’s relationship with the IMF deepened after the 2016 economic reform program, which included significant devaluation of the Egyptian pound and subsidy reforms. The country entered into a $3 billion agreement with the IMF in 2022 to address rising external financing needs.

– Argentina: Perhaps the most well-known IMF debtor, Argentina’s economic troubles have led to multiple IMF programs over the decades. The country’s $57 billion loan agreement in 2018 was the largest in IMF history, though Argentina has struggled to meet its obligations and has repeatedly sought debt restructuring.

2. Currency Devaluation and Inflation:

High inflation and repeated currency devaluations are common issues that have exacerbated the debt situations in these countries. Persistent inflation erodes purchasing power, while currency devaluation increases the burden of foreign-denominated debt.

– Pakistan: The Pakistani Rupee has experienced severe depreciation over the past few years, losing over 50% of its value against the US dollar since 2020. Inflation has remained in double digits, with food and energy prices particularly hard hit.

– Egypt: The Egyptian pound has undergone several devaluations, especially after 2016, when the government floated the currency as part of the IMF deal. Inflation surged in response, with food inflation reaching alarming levels in recent years.

– Argentina: Argentina’s economic history is marred by hyperinflation and continuous currency crises. The Argentine peso has lost much of its value, and inflation rates in 2023 exceeded 100%. This chronic inflation is a key reason for Argentina’s recurring financial crises.

3. Structural Economic Challenges:

All three countries face structural economic issues, including large fiscal deficits, inefficient public sectors, and low levels of foreign direct investment (FDI). These problems contribute to their inability to generate enough domestic revenue to service their debts, making them reliant on external borrowing.

– Pakistan: Chronic fiscal deficits, driven by low tax revenue and high defense and debt servicing costs, have led to continuous borrowing. Structural issues like low industrial productivity, a large informal economy, and energy shortages compound the problem.

– Egypt: Egypt’s economic growth has been hampered by a large and inefficient public sector, significant subsidies on food and fuel, and political instability. While the government has undertaken reforms, progress has been slow, and debt servicing remains a significant burden.

– Argentina: Argentina’s history of populist economic policies, including heavy subsidies, price controls, and protectionism, has led to fiscal imbalances and recurrent debt crises. Political instability and a lack of investor confidence have further exacerbated these issues.

4. Geopolitical and Social Instability:

Geopolitical risks and social unrest have been significant factors in the economic instability of these countries. Social unrest often results from austerity measures required by international lenders, leading to further economic and political instability.

– Pakistan: Ongoing geopolitical tensions, especially related to security issues, have placed significant strain on the country’s finances. Social unrest has also grown as austerity measures have led to higher prices and reduced subsidies.

– Egypt: Political unrest following the 2011 revolution and subsequent political transitions have caused economic disruptions. Social tensions remain high, especially with the implementation of IMF-mandated reforms that have raised the cost of living.

– Argentina: Argentina’s history of political instability, including frequent changes in government, has contributed to its economic woes. Austerity measures required by debt renegotiations often lead to public protests, further complicating governance and economic management.

Conclusion

Pakistan, Egypt, and Argentina, though geographically and culturally distinct, face strikingly similar economic challenges, particularly in managing their debt burdens. Reliance on external financing, currency devaluation, inflation, and structural economic issues are common threads in their economic stories. While each country’s specific circumstances differ, the overarching theme is one of struggling to balance economic growth with the heavy weight of debt obligations.

For these countries, addressing their debt issues will require not only short-term stabilization measures but also long-term structural reforms. Diversifying economies, improving tax collection, enhancing productivity, and fostering political stability are critical to breaking the cycle of debt dependence. As these nations navigate their economic futures, the lessons learned from their shared experiences may offer valuable insights into the path forward.